Good Morning,

U.S. stocks rebounded on Friday as Wall Street reassessed concerns arising from news that the White House could seek a hike to the capital gains tax.

On Thursday markets had a volatile session after multiple news outlets reported that President Joe Biden is slated to propose much higher capital gains taxes for the rich.

Bloomberg News reported that Biden is planning a capital gains tax hike to as high as 43.4% for wealthy Americans.

The proposal would hike the capital gains rate to 39.6% for those earning $1 million or more, up from 20% currently, according to Bloomberg News, citing people familiar with the matter. Reuters and the New York Times later also reported similar stories.

Still, with Democrats’ narrow majority control in Congress, a tax bill like this could face challenges and many on Wall Street believe a less dramatic increase is more likely.

We expect Congress will pass a scaled back version of this tax increase,” wrote Goldman Sachs economists in a note. “We expect Congress will settle on a more modest increase, potentially around 28%.”

Interestingly, U.S. taxable domestic investors own only about 25% of the U.S. stock market, according to UBS. The rest of the market is owned in accounts that aren’t subject to capital gains taxes such as retirement accounts, endowments and foreign investors, so the impact on overall stock prices should be limited even with a higher tax rate.

As earnings season is well underway, corporations have for the most part managed to beat Wall Street’s expectations. Still, strong first-quarter results have been met with a more tepid response from investors, who have not, to date, snapped up shares of companies with some of the best results. This is especially true of the reflation/cyclicals who continue to be 2021’s market’s darlings.

Our Take

What looked like a perfect downside setup last month didn't create anything more than a minor dip. The market certainly seems to have underlying strength to it with many sectors and assets hitting ATHs.

Nevertheless, the market is showing some signs of exhaustion, and with good reason. Most major parts of the market have run up significantly in the past month and there is a growing chorus warning that we are at “peak everything.” That is, peak earnings growth, peak economic data and peak reopening.

From our perspective, most assets look fully valued offering perhaps the lowest prospective returns we’ve ever seen. The easy money has likely been made. Growth (ISM) typically peaks around a year (10-11 months) after a recession ends, right at the point we would appear to be. A majority of historical peaks in growth (two thirds) were inverted-V shaped, while the rest saw the ISM flatten out at an elevated level. The S&P 500 sold off around growth peaks by a median -8.4%, but even episodes which saw the ISM flatten out rather than fall, saw a median -5.9% selloff.

When the ISM's manufacturing activity reading exceeds 60, the S&P 500 tends to be lower over the next three- and six-month periods. In March, the ISM's manufacturing activity index registered a reading of 64.7 (37-year high). Not to mention that global economic growth accelerated to the fastest in just over six and a half years in March and the IMF is forecasting world economic growth to be the best in forty years.

Everything the market discounted in 2020 is happening now, and so there's no obvious positive catalyst for markets over the next few quarters. Everyone, in other words, already knows what the most bullish story is right now for markets. And additional pieces of good news are unlikely to change the outlook for indexes that have already rallied 80% or more in a year.

Nevertheless, the resilient grind higher (strong market breadth and more than 75% of stocks above 200 SMA) that we've seen over the past couple of weeks is consistent with a bull market, and as long as things stay boring and support continues to hold, we don’t see any compelling reason to be out of the market. Furthermore, many of the “speculative sectors” have taken a beating of late which bodes well for future returns.

The global rollout of Covid-19 vaccines, the persistence of ultralow interest rates, and expectations for torrid economic growth should continue to provide a nice tailwind for the investor who holds a portfolio of “winner take most” businesses in the innovation space. Long-term investing remains a marathon of compounding that consists of countless sprints. As Morgan Housel has smartly remarked, there are books on economic cycles, trading strategies, sector bets and investment approaches yet the most powerful and important book should simply be called: “Shut Up and Wait.”

Musings

What was particularly exciting about this year's March technology selloff was the opportunity to evaluate smaller capitalization stocks set to benefit from significant structural changes in the economy trading at more reasonable prices. One such stock we purchased in the quarter is DMYI. DMYI is a SPAC launched by dmy Technology Group Inc. (one of the more reputable SPAC sponsors) that will soon merge with IonQ (will trade under the symbol IONQ). This will make IonQ the first ever publicly traded pure-play quantum computing business on the NYSE.

Why quantum computing?

"This is going to be the decade in which quantum really comes of age,” an IBM executive recently told the Wall Street Journal. Quantum computing is to AI what nuclear weapons are to bombs. Corporates, institutions and other entities are thus racing to build such a new type of computer, a quantum computer, that will bring the computational hardware required to match and exceed the human brain. This will require the computation of models 1,000x larger than OpenAI’s massive GPT3, or 100x larger than Google’s recent 1T parameter leviathan.

While quantum technology will take years to scale, the race is on to build the software and hardware infrastructure today. The race to such technology will be a defining theme of the decade to come and the stakes could not be higher. The current CEO of Google, Sundar Pichai, has said that the impact of AI will be more profound than man’s discovery of fire. Palantir’s CEO recently stated that:

“Military AI will determine our lives, the lives of your kids. This is a zero-sum thing. The country with the most important AI, most powerful AI, will determine the rules. That country should be either us or a Western country.

That doesn't mean you're anti-our-adversaries. It just means would you rather have them with the equivalent of tech nuclear arms or us?

This program will quite literally determine who is standing here [at Davos] and what they're saying in five years.”

If (in the words of Ray Dalio) the Federal Reserve’s printing press is the world’s most valuable asset, the world’s first scaled-up quantum computer and/or generally intelligent AI would be a close second.

Enter IonQ. IonQ started as a research project about 10 years ago (as a business about 6 years ago) by Chris Monroe (head of quantum physics at the University of Maryland, College Park) and Jungsang Kim (Professor of Quantum Physics and Electrical Engineering at Duke University, formerly of Bell Labs) who wanted to build the most powerful quantum computer using trapped ytterbium atoms, a unique method that reduces the overall space required to create a quantum computer without seeing loss in quantum power.

This is an interesting method because unlike other methods (ie. those done by Google, IBM, Rigetti etc.), the trapped-ion method comes from nature and builds quantum qubits on a small chip (Honeywell who also realized the power of quantum is also using an ion method). Despite the other methods of building a quantum computer, there are several unique advantages of the trapped-ion method including low error correction, high gate fidelity, scalability (although scalability overall is still an issue), noise reduction and lower costs to operate (other methods require tremendous electrical and refrigeration costs).

The reason IonQ has gained traction and attracted capital is three-fold: 1. IonQ has the most advanced quantum method on quantum volume alone; 2. They have attracted the best business and technical minds of any quantum computing business to date; and 3. Their long-term business model revolves around Quantum Computing as a Service and managed services (their QCaaS currently charges roughly $10 per compute hour on AWS and Azure). On the talent front, both Mr. Monroe and Mr. Kim are two of the best minds in quantum physics and have both a combined over 51,000 academic citations in the area. In fact, Dave Bacon, who was head of Google’s quantum division and one of the authors of the Bacon-Shor quantum algorithm, left Google to join IonQ. Peter Chapman is the current CEO of IonQ (former MIT grad and son of a NASA astronaut) and is the former head of engineering at Amazon Prime.

From a capitalization perspective, the business raised $650 million (roughly $350 million in a PIPE and $300 million through the SPAC) at an enterprise value of $1.95bn ($10/share for DMYI). Although not an exhaustive list, the PIPE investors include some of the biggest investors in the world: Breakthrough Energy (Bill Gates), TIME Ventures (Marc Benioff), MSD Capital, Silver Lake Partners, Fidelity and Hyundai. Existing investors include but are not limited to Amazon Web Services, Bosch, Samsung Ventures, Tao Capital, Lockheed Martin, Airbus Ventures and HPE Ventures. Currently, the business’s quantum service is the only one available on both AWS and Azure and once merged, they will end up being the most well-funded standalone quantum business. Their investor base will also be the business’s first customers (Samsung, HPE and Airbus have already publicly committed to using their services for real-world applications) and Dow Chemical has recently used their service to recreate the water molecule.

Despite our excitement about IonQ’s prospects, this is a very long-term investment for the LP as there will be multiple phases before we see broad commercial use of quantum computing (early on its S-curve growth runway). There are still significant technical barriers to the technology, the most important being error correction, error modification and scalability. Currently, the ion-trap method uses a significant number of lasers to manipulate the ytterbium atom, which is something that is not sustainable long-term. These technical barriers must be fixed and enhanced over the next few years before they can use their technology for broader commercial applications. From a business perspective, we will need to see the creation of a flywheel over time (acquisition of software, security services, developer portals etc.) to continue to attract talent and provide top notch customer service, just like Amazon has with AWS.

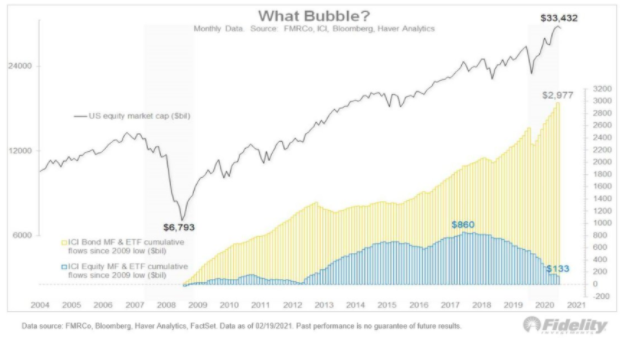

Charts of the Month

Human innovation always trumps fear.

Private equity (PE) deal valuations by EV/EBITDA are increasingly rich and are hitting higher double-digit figures.

2021 is expected to be another home run year for PE, with 20% of buyouts estimated to be priced above 20x EV/EBITDA.

Logos LP March 2021 Performance

March 2021 Return: -14.71%

2021 YTD (March) Return: -1.96%

Trailing Twelve Month Return: 126.85%

Compound Annual Growth Rate (CAGR) since inception March 26, 2014: 24.09%

Thought of the Month

“Remember to conduct yourself in life as if it was a banquet. As something being passed around comes to you, reach out your hand and take a moderate helping. Does it pass you by? Don’t stop it. It hasn’t yet come? Don’t burn in desire for it, but wait until it arrives in front of you. Act this way with children, a spouse, toward position, with wealth - one day it will make you worthy of a banquet with the gods.” - Epictetus, Enchiridion, 15

Logos LP Services

Looking for portfolio construction support? We would be happy to chat. Please book an intro call here.

Articles and Ideas of Interest

There’s a name for the Blah you’re feeling: It’s called Languishing. Colleagues reported that even with vaccines on the horizon, they weren’t excited about 2021. A family member was staying up late to watch “National Treasure” again even though she knows the movie by heart. And instead of bouncing out of bed at 6 a.m., I was lying there until 7, playing Words with Friends. It wasn’t burnout — we still had energy. It wasn’t depression — we didn’t feel hopeless. We just felt somewhat joyless and aimless. It turns out there’s a name for that: languishing. Languishing is a sense of stagnation and emptiness. It feels as if you’re muddling through your days, looking at your life through a foggy windshield. And it might be the dominant emotion of 2021.

Welcome to the YOLO economy. Burned out and flush with savings, some workers are quitting stable jobs in search of postpandemic adventure. The NYT reports that some are abandoning cushy and stable jobs to start a new business, turn a side hustle into a full-time gig or finally work on that screenplay. Others are scoffing at their bosses’ return-to-office mandates and threatening to quit unless they’re allowed to work wherever and whenever they want. If “languishing” is 2021’s dominant emotion, YOLOing may be the year’s defining work force trend. A recent Microsoft survey found that more than 40 percent of workers globally were considering leaving their jobs this year. Blind, an anonymous social network that is popular with tech workers, recently found that 49 percent of its users planned to get a new job this year.

WOKEISM – The New Religion of the West. There is a new religion. It is moving like a tidal wave through every facet of western culture, shaping and redefining society as it goes. This religion masquerades under the guise of compassion and justice, but underneath is an evil ideology that is incompatible with western values and incongruent with the Christian worldview. This movement did not start in Minneapolis on May 25th, when George Floyd was murdered. That event acted as a watershed moment for an ideology that has been growing for decades. If left unchecked, this new religion could lead to a complete unravelling of western culture. There are many names for what we currently find ourselves in; wokeness, political correctness, and cancel culture are some of them, but these only encapsulate a portion of the phenomenon. Cultural Marxism, neo-marxism, social justice, identity politics, and Critical Theory are broader descriptors. We would like to use a term that adequately captures the religiosity of the movement: wokeism.

The economics of falling populations. The Economist explores how a shrinking global population could slow technological progress. While Joel Kotkin reminds us to be careful for what we wish for as declining fertility rates may deliver us into oblivion. We could choose to create a kind of woke utopia, where children and families are rare, upward mobility is constrained, and society ruled by a kind of collective welfare system that rewards inactivity and stagnation. But to those who value the permanence of our society, and the remarkable importance of children, this is something close to a dystopia. To be sure, a smaller, older society may emit fewer greenhouse gasses per capita, but at the end we confront a society that will be less innovative, less dynamic and, in the most profound sense, distinctly less human.

Neurotechnology could one day shape our thoughts and behaviors. Scientists have discovered how to use technology to put an artificial image inside a mouse's brain so that it behaves as if it actually sees it. This will be possible to do with humans in the future — potentially shaping our thoughts and behaviors.

Millions are tumbling out of the global middle class in historic setback. An estimated 150 million slipped down the economic ladder in 2020, the first pullback in almost three decades.

Europe is heading toward a new financial crisis. Europe faces a predicament. Even as it struggles to contain the Covid-19 pandemic, it’s setting itself up for another crisis — this one financial. To ensure the viability of the common currency at the heart of the European project, the EU’s leaders will have to cooperate in ways they’ve so far resisted.

Turkey’s crypto pain grows with second exchange collapse. Turkey’s cryptocurrency investors were dealt another blow at the end of a dismal week after a second big exchange collapsed in as many days and its chief executive was reportedly detained. We expect regulators to increase their scrutiny of this asset class. Betting on Bitcoin? You should know the story of the Hunt brothers and the silver market. It was arguably the biggest business story of 1980. Two of the world’s richest men, Texans Bunker and Herbert Hunt––along with Saudi partners––had bought or amassed contracts to purchase over three-quarters of the world’s silver in private hands. Speculators jumped on the news, driving the price to never-before-seen peaks. Then the commodities exchanges panicked and banned selling, the Fed pushed the banks to call the Hunts’ gigantic loans, and strip mall storefronts lured folks to sell their bracelets and silverware to be melted into bullion, flooding the market with the precious metal. In just five months, silver’s price cratered 80%, scorching the billionaire brothers’ fortunes. Seldom in financial history has America witnessed a craze where so much wealth mushroomed then disappeared in such a brief span, or one featuring a cast of such colorful, damn-the-establishment mavericks.

Microsoft’s $20 billion AI deal will shake up how we work. The technology giant’s purchase of voice-recognition and AI specialist Nuance Communications puts it at the forefront of the next big wave of workplace innovation. Imagine the workplace of the future, where computers powered by artificial intelligence take care of the most tedious administrative tasks, making employees happier and more productive. Microsoft Corp. wants to be at the forefront of that future — and its deal for voice-recognition and AI specialist Nuance Communications Inc. shows it’s willing to spend a lot of money to do it.

Our best wishes for a month filled with joy and contentment,

Logos LP