Good Morning,

Stocks gyrated between gains and losses Friday to end a volatile week on Wall Street, as investors appeared content to consolidate positions after worries over Evergrande and a slowing global economy prompted traders to pull $28.6 billion from U.S. equity funds over the first three days of the week, the most since February 2018. But stocks then staged a two-day rally after the Federal Reserve signaled no removal of its easy money policy, at least for now.

Tech stocks trailed Friday after a crackdown on bitcoin by China overnight hurt sentiment in the sector, but financial stocks rose as the 10-year U.S. Treasury yield reached its highest since July. "What is clear is that inflation is likely to be the determining factor for liftoff and the pace of rate hikes," Deutsche Bank Chief U.S. Economist Matthew Luzzetti wrote in a note. "If inflation is at or below the Fed's current forecast next year of 2.3% core PCE, liftoff is likely to come in 2023, consistent with our view. However, if inflation proves to be higher with inflation expectations continuing to rise, the first rate increase could well migrate into 2022."

Meanwhile Nike confirmed investor concerns about the pandemic wreaking havoc with supply chains and raising costs for companies, especially multinationals. Nike shares fell 6.2% after the sneaker giant lowered its fiscal 2022 outlook because of a prolonged production shutdown in Vietnam, labor shortages and lengthy transit times.

Our Take

Skepticism on Wall Street is widespread with most of the major investment firms calling for a 10-20% market correction. Furthermore, the popular narrative for the rest of the year appears to be falling Covid cases globally and economic acceleration favouring cyclical stocks in the energy, financial, industrial and travel sectors. For us the data is noisy. Economic acceleration could very well occur but we also believe as we have stated in the past, that there are equally compelling reasons to infer significant economic deceleration.

At present we believe policy error in the form of excessive government intervention in the economy to be the largest risk to growth estimates. Several countries closely regulate industries, labor, and markets, set monetary policy, and provide subsidies to help boost their economies yet many countries are veering towards giving the government a level of control that would allow it to steer the economy and industry along a path of its exact choosing channeling additional private resources into strengthening state power.

The big risk for these countries is that the push winds up suppressing much of the entrepreneurial energy and incentives that have powered their boom, years of innovation and improving standards of living.

From a market standpoint, we continue to believe that as pandemic-era programs to bolster the economy are lifted there will be an easing of market conditions which favor the indexes and tech megacaps. The era of narrow stock leadership -- powered by the explosive growth in passive funds -- may be beginning to unwind. Less aggressive monetary easing ahead should expand the number of market winners favoring active management. PanAgora Asset Management’s research suggests that a cap-weighted strategy thrives as concentration rises, but delivers “significantly” lower returns when the macro climate shifts in favor of higher rates.

The removal of policy supports could mean the fundamentals of individual companies come to the fore replacing what has been a wall of stimulus money hitting the indexes. We see much opportunity for outperformance ahead...

Musings

Over the past month, as I’ve watched politicians worldwide flounder around on everything from public health, housing, the economy, taxation to capitalism itself I’ve found myself thinking more about my framework for viewing life and investing. The future is becoming more and more uncertain as the world is changing rapidly while those in power appear less and less capable of leading with grace and conviction. It is possible we are at the dawn of the period of greatest change for the past few centuries and the range of potential outcomes when pondering the coming decade or two spans from “dystopia to Renaissance”.

In Canada and across the border in the USA, our democracies appear to be in the hands of statists who believe that government justifiably holds near-absolute power. During the recent Canadian election and the ongoing Democrat proposed 3.5T spending discussions there is little sense that there are or should be limits on the power of democratically elected governments. Such limits still exist in constitutional form, but they are being overwhelmed in spirit if not in law. A tax on wealth and capital? Previously unimaginable spending and deficits? Restrictions on the right to buy and sell property? Restrictions on speech, employment, movement and association based on “woke” ideological purity? Break up corporations? State led discriminatory attacks on certain corporations and individuals based on their ability to make profits? No worries. Big brother knows best and more government intervention and control is warranted.

The overall ideological thread today has been that governments have the power and the right to do whatever they want — a trend that COVID-19 appears to have entrenched globally.

Authoritarianism is on the rise around the world with governments becoming less transparent and losing the people's trust. The latest report 'Freedom in the World 2021' by Freedom House is sobering. The report, which is an annual country-by-country assessment of political rights and civil liberties, downgraded the freedom scores of 73 countries, representing 75 per cent of the global population. Democracy has eroded in the United States as well, the report noted.

While still considered 'free', the United States has experienced further democratic decline. The US score in 'Freedom in the World' has dropped by 11 points over the past decade, and fell by three points in 2020 alone.

How much of the above is in our control? The rules of the game keep shifting as the state increasingly imposes its will on markets, society and culture. Watching this distressing reality unfold, largely out of my control, has prompted me to think more deeply about my framework for viewing life and investing.

As a starting point, William Green in his fantastic new book suggests that it’s helpful to view investing and life as games in which we must consciously and consistently seek to maximize our odds of success. The rules are slippery and the outcomes unpredictable yet there are intelligent ways to play as well as stupid ones.

How can we avoid swimming upstream and instead be carried with the current? How do we tilt the odds in our favor regardless of the environment or “playing field”?

When it comes to investing, much ink has been spilt on this. Without diving too deeply we could distill the common “get an edge” formula into the following principles:

Be patient and selective exploiting neglected and misunderstood market niches.

Say no to almost everything.

Exploit the market’s bipolar mood swings.

Buy companies at a discount to their intrinsic value.

Stay within your circle of competence.

Filter out the noise, keep things simple and avoid anything too complex.

Make a small number of bets with minimal downside and high upside.

Control your emotions and be patient.

Simple but not always easy to follow. But my goal here isn’t to review the core principles that most investors likely already know, or should know.

Instead, faced with the increasingly frustrating and downright depressing global macro political environment I tried to think about the times in my investing career I was best able to follow the above principles.

What I found was that essentially all of the moments I had achieved some sort of “high performance” or “success” occurred in periods of time in my life in which I was joyous. Periods of time when I was particularly happy.

Interestingly, perhaps the most consistent way we can maximize our odds of success is adopting an optimistic and positive attitude. Shawn Achor in his fascinating book “The Happiness Advantage” explains that “waiting to be happy limits our brain’s potential for success, whereas cultivating positive brains makes us more motivated, efficient, resilient, creative, and productive, which drives performance upward.”

New research in psychology and neuroscience demonstrates that we become more successful when we are happier and more positive. In his book, Achor outlines that: “doctors put in a positive mood before making a diagnosis show almost three times more intelligence and creativity than doctors in a neutral state, and they make accurate diagnoses 19 percent faster. Optimistic salespeople outsell their pessimistic counterparts by 56 percent. Students primed to feel happy before taking math achievement tests far outperform their neutral peers.”

Unfortunately, for most of us, we are conditioned from birth to believe that once we become successful then we will be happy. Success is conceptualized as a necessary condition for happiness. If we get the promotion/raise/car/return [insert success/external validation], we will be happy. But with each victory the goals shift and the happiness gets pushed further out.

Instead, in the face of an increasingly precarious future including its associated “FUD: Fear, Uncertainty and Doubt” I think that focusing on happiness as a precursor to success rather than simply its result is game changing. This kind of relationship with happiness is the ultimate way we can tilt the odds in our favor in investing and perhaps more importantly in life.

Anytime you get a truth that much of humanity doesn’t understand, that’s a large competitive advantage. Intelligent people are easily seduced by complexity while underestimating the importance of simple ideas that carry enormous weight. When you consistently apply a powerful idea such as the happiness advantage with thoughtful diligence, the effects may astonish you...

Charts of the Month

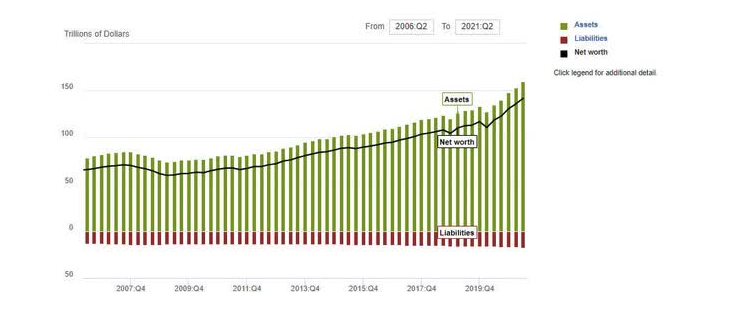

According to the Fed's Z.1 report, U.S. Household net worth rose at a solid 18.4% rate in Q2 to $142 Trillion, after gains of 16.7% in Q1 and 28.5% in Q4 '20. The "Wealth Effect" is one of the most important statistics we can use to measure how American households are faring. This measurement leads to the "feel good" effect that adds to the confidence to go out and spend. It is comical that this report never makes a headline. Then again the popular rhetoric is still concentrating on how BAD things are out there. The data on consumers doesn’t seem to support that outlook...

Men are falling behind remarkably fast, abandoning higher education in such numbers that they now trail female college students by record numbers. No one is talking about it.

Logos LP August 2021 Performance

August 2021 Return: 10.23%

2021 YTD (August) Return: 18.26%

Trailing Twelve Month Return: 57.07%

Compound Annual Growth Rate (CAGR) since inception March 26, 2014: 25.71%

Thought of the Month

“The very purpose of religion is to control yourself, not to criticize others. Rather, we must criticize ourselves. How much am I doing about my anger? About my attachment, about my hatred, about my pride, my jealousy? These are the things that we must check in daily life.” -Dalai Lama.

Articles and Ideas of Interest

ESG is inflationary. As the global economy rebounds, the likelihood of inflation has become the dominant economic story. You can’t watch the financial news for long without hearing about inflation. At the same time, environmental, social, and governance (ESG) initiatives continue on an inexorable march to greater public perception. However, despite both issues occupying ever more column inches, one consideration has been underexplored; ESG will add to inflationary pressures. TwentyFour Asset Management suggests that yes, ESG is a new source of inflation that was not so present in the previous cycle and cannot be overlooked when forming a view on this cycle’s inflation outlook. How willing will consumers be to shoulder such rapidly increasing costs? There's arguably a point at which a preponderance of inflationary pressures may backfire, with people suddenly demanding governments do something (anything!) to ensure access to cheaper energy (never mind whether it's dirty or not)...Britain looks set to bump up against this reality as some customers are facing a 50% increase in their energy bills…

Replicating private equity with liquid public securities. According to a Harvard Business School study, it is possible to replicate private equity returns with liquid public securities. “A passive portfolio of small, low EBITDA (earnings before interest, taxes, depreciation, and amortization – a commonly used measure of cash flow) multiple stocks with modest amounts of leverage and hold-to-maturity accounting of net asset value produces an unconditional return distribution that is highly consistent with that of the pre-fee aggregate private equity index.” Accelerate in a fascinating report believes that Harvard has it right, despite claims from private equity executives insisting otherwise.

Lie Flat’ if you want, but be ready to pay the price. The new “lie flat” social protest movement seems to be catching on. It started among overworked Chinese factory workers burned out from grueling 12-hour, six-day work weeks, and the unrelenting pressure from the government and society to climb the economic ladder. So some Chinese millennials formed an underground movement to opt out of work and the pressures of society. Never ones to miss a chance to cry “hardship,” upper-middle-class, well-educated young Americans are also getting in on the action, claiming they, too, are burned out and quitting their jobs to do nothing. What this trend will mean for China is unclear, but Allison Schrager suggests that Americans who choose to lay down in lieu of work may end up worse off than they think.

The ‘melancholic joy’ of living in our brutal, beautiful world. Brian Treanor writes that it’s a challenging time to be an optimist. Climate change is widespread, rapid and intensifying. The threat of nuclear war is more complex and unpredictable than ever. Authoritarianism is resurgent. And these dangers were present even before we were beset by a historic pandemic. The data clearly show that based on certain objective measures of wellbeing we are living in the best of times – yet many people feel dissatisfied. In some places, including the US, self-reported happiness has actually been on the decline. So how should we view the state of the world: with optimism or pessimism? In answering, Treanor suggests that we must contemplate the broad sweep of both the world’s goodness and its evils.

The everything bubble and TINA 2.0. FTX research does an fantastic job of exploring that common statement that “We are in an everything bubble” reviewing the data and going asset by asset. Worth the read. Spoiler: There’s most certainly pockets of excess in nearly every corner of the financial markets, but there’s also ample opportunity.

Why is gold not rising? Interesting take on the shiny metal (albeit from a gold bug) via GoldSwitzerland.

Silicon Valley is searching for the fountain of youth in a bill. Human aging is the latest and greatest field being disrupted by technology. The big picture: Work on therapeutics that could slow or even prevent the aging process is moving out of the fringes and into the mainstream, fueled by funding from tech billionaires who have one thing left to conquer: death.

What if people don’t want a career? Charlie Warzel, a reporter on the future of work has found an interesting and potentially profound trend: the growing skepticism around ‘careers.’ ‘Careerist’ has long been a dirty word in the working world — usually it’s meant to signify a cynical, ladder climbing mentality. A careerist isn’t a team player. They care more about the job title and advancement than the work. The current brand of career skepticism he is talking about is different, more absolute. It’s not a rejection of how somebody navigates the game, it’s a rejection of the game itself. The idea isn’t limited to a specific age group, but the best articulation of it comes from younger Millennials and working age Gen Zers. Many of them are fed up with their jobs and they’re quitting in droves. Even those with jobs are reevaluating their options. What comes next?

You are living in the Golden Age of stupidity. The convergence of many seemingly unrelated elements has produced an explosion of brainlessness. Interesting take by Lance Morrow suggesting that stupidity dominates in our time because of a convergence of seemingly unrelated elements (the death of manners and privacy) that - mixed together at one moment, in our cultural beaker - have produced a fatal explosion.

Why you need to protect your sense of wonder - especially now. As the pandemic era goes on, more than ever we need ways to refresh our energies, calm our anxieties, and nurse our well-being. The cultivation of experiences of awe can bring these benefits and has been attracting increased attention due to more rigorous research. At its core, awe has an element of vastness that makes us feel small; this tends to decrease our mental chatter and worries and helps us think about ideas, issues, and people outside of ourselves, improving creativity and collaboration as well as energy. David Fessell and Karen Reivich, a physician and a psychologist, have facilitated hundreds of resilience and well-being workshops; they suggest for HBR a number of awe interventions for individual professionals as well as groups.

Our best wishes for a month filled with joy and contentment,

Logos LP