Good Morning,

The tech-heavy Nasdaq composite rose to a record high last Friday as Wall Street cheered the blowout quarterly reports from three of the world's biggest tech companies.

The index rose 2.2 percent to 6,701.26 and notched its biggest one-day gain since November 2016.

The PowerShares QQQ Trust exchange-traded fund, which tracks the Nasdaq 100, rose 2.9 percent.

Leading the ETF higher were shares of Amazon, Microsoft and Google-parentAlphabet; their stocks rose 13.2 percent, 6.4 percent and 4.3 percent, respectively.

The S&P 500 Index also hit a new high, after the U.S. saw its strongest consecutive quarters of growth in gross domestic product in three years.

The first reading on third-quarter GDP showed the U.S. economy grew by 3 percent, above an estimate of 2.5 percent indicating resilient demand from consumers and businesses even with the hit from hurricanes Harvey and Irma, Commerce Department data showed Friday. In addition, U.S. consumer sentiment rose to its highest level since 2004.

Our Take

These tech giants reported excellent numbers. Amazon's third-quarter earnings stole the show with accelerating revenues, a growing customer base, 42 percent sales growth in Amazon Web Services and a busy Prime Day.

Alphabet's earnings report impressed thanks to its 70 percent growth in YouTube, which now delivers 100 million hours of content per day to its users.

Microsoft blew away Wall Street's earnings estimates by delivering 42 percent growth in subscription revenue from its Office 365 offering and 90 percent revenue growth from Azure, its cloud platform.

This tech strength is closely tied to the growing importance of data. More specifically, the explosion of data via the cloud. Amazon, Alphabet and Microsoft are the big three of web services, the backbone of the cloud. Expect the strength to continue as these giants continue to shore up their dominant positions in the space.

For Q3 2017, with 55% of the companies in the S&P 500 reporting actual results for the quarter, 76% of S&P 500 companies have reported positive EPS surprises and 67% have reported positive sales surprises.

For Q3 2017, the blended earnings growth rate for the S&P 500 is 4.7%. Six sectors are reporting earnings growth for the quarter, led by the Energy sector. On Sept. 30, the estimated earnings growth rate for Q3 2017 was 3%.

These are excellent numbers supporting the suggestion that this is a rally based on earnings growth.

A very strong bull market indeed, also supported by a global economy that continues to surprise to the upside.

Even Caterpillar earnings which showed increased profits and and improved outlook which tends to evidence that global growth is picking up in a synchronized fashion.

Valuations continue to look frothy but fundamentals are keeping pace.

As we have previously stated, caution is warranted in this environment yet caution should also be exercised when faced with arguments that both the economic cycle and the stock market has run its course and it is time to lighten up, raise cash and wait for an imminent crash.

The veracity of these types of arguments now seems obvious. The danger is believing that what seems obvious, must take place. This is simply untrue. Instead, such beliefs evidence the primacy of emotion over reason. A lazy reliance on heuristic shortcuts rather than thoughtful analysis.

The skeptics have and continue to beat their drums yet the place to be remains equities. The brightest opportunity for returns over the long-term remains the ownership of high quality businesses.

Musings

Thought-provoking piece in HBR I came across this week which suggests that in a distracted world, solitude is now a competitive advantage. “Always remember: Your focus determines your reality.” Jedi Master Qui-Gon Jinn shares this advice with Anakin Skywalker in Star Wars, but in our hyper-distracted work world, it’s advice that we all need to hear.

Research by the University of London reveals that our IQ drops by five to 15 points when we are multitasking. In his book, Your Brain at Work, David Rock explains that performance can decrease by up to 50% when a person focuses on two mental tasks at once.

Our world is becoming increasingly complex which is having a major impact on our lives especially when it comes to problem solving. Pushed and pulled by X,Y and Z stimulus at any given time it is unclear how we can solve the challenges of our age. The answer may lie in cultivating solitude.

Having the discipline to step back from the noise of the world is essential to staying focused and thus to staying effective.

How can we cultivate solitude? How can we build this skill?

Build periods of solitude into your schedule

Analyze where your time is best spent

Starve your distractions

Don’t be too busy to learn how to be less busy

Create a “stop doing” list

Logos LP September Performance

September 2017 Return: 2.03%

2017 YTD (September) Return: +15.57%

Trailing Twelve Month Return: +18.71%

CAGR since inception March 26, 2014: +18.06%

Thought of the Week

"I’m a “dumb shit” who doesn’t know much relative to what I need to know. Whatever success I’ve had in life has had more to do with my knowing how to deal with my not knowing than anything I know.” - Ray Dalio

Articles and Ideas of Interest

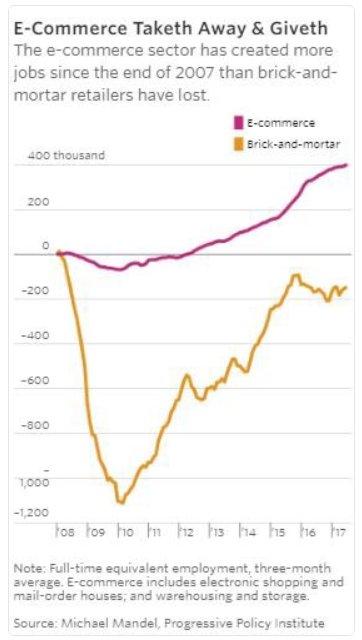

- These are the businesses still immune to Amazon. In order of least likely:1) Dollar Stores 2) Auto parts 3) Home improvement 4) Home Furnishing

- Our biggest economic, social and political issue The Two Economies: The Top 40% and the Bottom 60%. Very interesting piece from Ray Dalio suggesting that Average statistics camouflage what is happening in the US economy, which could lead to dangerous miscalculations, most importantly by policy makers. For example, looking at average statistics could lead the Federal Reserve to judge the economy for the average man to be healthier than it really is and to misgauge the most important things that are going on with the economy, labor markets, inflation, capital formation, and productivity, rather than if the Fed were to use more granular statistics.

- Tim O’Reilly: ‘Generosity is the thing that is at the beginning of prosperity’. Tech pioneer and CEO Tim O’Reilly suggests that his industry will fail unless the web giants start putting consumers ahead of shareholders. When questioned about the notion that technology is going to eliminate jobs, Tim counters by suggesting that this will happen only if that’s what we tell it to do. And it is what we’re telling it to do. But on the other hand Marc Bain suggests that now corporations kneel down to us. We’re in the midst of a profound shift in consumer culture, he writes. Corporations were once king, but “influencers” and viral videos—like the one of the United Airlines passenger-dragging incident that shaved $1 billion off the company’s valuation—have shifted the balance of power. A new report examines how US buying behavior will change as a result. Nobel Prize winner Joseph E. Stiglitz writes that America has a huge monopoly problem.

Robots are eating money managers’ lunch. Rishi Ganti on why obscure assets may be the human investor’s last refuge. Like what? Like scooping up receivables and other claims owed to those in need of immediate cash—a refugee facility waiting for payment on a contract from a charity, for example. Luckily robots still have a lot to learn about being a human trader.

- How social media endangers knowledge. The very idea of knowledge itself is in danger. The idea behind Wikipedia—like all encyclopedias before it—has been to collect the entirety of human knowledge. It’s a goal that extends back to the Islamic Golden Age, when numerous scholars—inspired by Muhammad's famous verdict of ‘Seek knowledge, even from China’—set themselves to collecting and documenting all existing information on a wide variety of topics, including translations from Greek, Persian, Syrian, and Indian into Arabic. Social networks, though, have since colonized the web for television’s values. From Facebook to Instagram, the medium refocuses our attention on videos and images, rewarding emotional appeals—‘like’ buttons—over rational ones. Instead of a quest for knowledge, it engages us in an endless zest for instant approval from an audience, for which we are constantly but unconsciously performing.

- Why is everyone so busy? Time poverty is a problem of perception and partly of distribution. The Economist looks into the fact that everybody, everywhere seems to be busy. In the corporate world, a “perennial time-scarcity problem” afflicts executives all over the globe, and the matter has only grown more acute in recent years, say analysts at McKinsey, a consultancy firm. These feelings are especially profound among working parents. As for all those time-saving gizmos, many people grumble that these bits of wizardry chew up far too much of their days, whether they are mouldering in traffic, navigating robotic voice-messaging systems or scything away at e-mail—sometimes all at once.

- Will Canadians survive higher rates? A new poll from Canada’s largest insolvency firm, MNP LTD, shows that 1 in 3 Canadians say that they already feeling the effects of increasing interest rates. Don’t think this is surprising considering well known debt issues. But that 63% of Canadians are either worried about bankruptcy or already feeling the effects of 50bps (to 1%)…feels like something that should be concerning.

Our best wishes for a fulfilling week,

Logos LP